What the UK’s Proposed Payment Reforms Could Mean for Treasury and Working Capital Strategies

The UK government’s proposed late payment reforms represent one of the most significant changes to corporate payment practices in more than 25 years.

Following a 2025 consultation and confirmation by the Government in March 2026, the proposed legislation aims to strengthen protections for small and medium-sized enterprises (SMEs) by limiting payment terms, increasing enforcement powers, and introducing mandatory interest on late payments.

If implemented, these changes could have important implications for treasury teams, particularly those that rely on supplier payment terms as part of their working capital strategy.

Key Proposed Legislative Measures

- 60-Day Hard Cap on Payment Terms: A maximum 60-day payment term is expected to be introduced for many B2B transactions involving SMEs, replacing the current “grossly unfair” test. The Government has also indicated that the cap could potentially reduce further to 45 days following a five-year transition period.

- Mandatory Interest on Late Payments: Statutory interest of 8% above the Bank of England base rate is proposed to become mandatory. Businesses would no longer be able to contract out of these provisions, making interest charges automatic when payments are made late.

- Enhanced Small Business Commissioner Powers: The Small Business Commissioner (SBC) is expected to receive expanded authority, including the ability to:

- Investigate poor payment practices using public or anonymous information

- Arbitrate payment disputes outside the court system

- Impose financial penalties on persistent late payers

- Board-Level Accountability: Large organisations with poor payment performance may be required to publicly explain their payment practices and disclose actions being taken to improve them.

Implementation and Scope

The legislation is expected to be introduced when Parliamentary time permits, with the 60-day payment cap unlikely to take effect before 2027.

Current proposals suggest exemptions may apply where:

- Both parties are large businesses

- The purchaser is smaller than the supplier

- Transactions involve imported or exported goods

The reforms are expected to affect UK-based buyers and suppliers, as well as organisations that transact with UK SMEs, making the proposed changes relevant for both domestic and international businesses operating within UK supply chains.

As with all proposed legislation, the final scope and implementation timeline remain subject to parliamentary approval.

What Treasury Leaders Should Consider

Once these reforms are enacted, it will significantly reduce flexibility around supplier payment terms for many organisations that buy from or supply UK-based SMEs.

As a result, treasury teams will need to reassess:

- Existing supplier payment term strategies

- Working capital optimisation programmes

- Supply chain finance structures

- Liquidity forecasting assumptions

- Alternative approaches to preserving cash flow

For businesses that have historically relied on extending payment terms to improve working capital, these changes will require a different approach.

While the final details are still evolving, organisations with significant SME supplier populations would benefit from evaluating potential impacts now rather than waiting for terms legislation.

How Treasury Teams Can Preserve Working Capital

As payment term flexibility becomes more restricted, organisations will increasingly explore solutions that separate supplier payment timing from buyer payment timing.

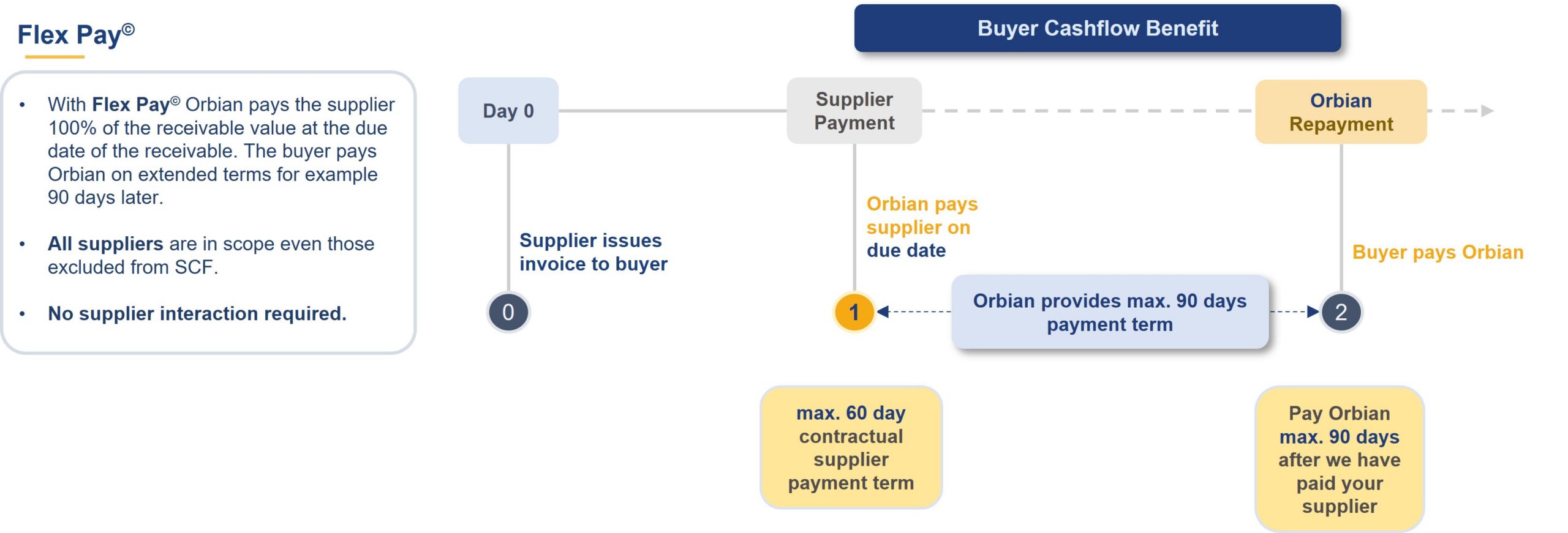

One example is Orbian’s Flex Pay© solution.

Flex Pay© enables:

- Suppliers to continue receiving payment on their agreed due date

- Buyers to access additional payment terms through Orbian

- Working capital optimisation without supplier onboarding or contract renegotiation

- Integration alongside existing payable finance or supply chain finance programmes

- Rapid implementation with minimal operational disruption

By maintaining supplier payment performance while providing additional payment flexibility to buyers, solutions such as Flex Pay© may help organisations adapt to a changing regulatory environment without disrupting supplier relationships.

Looking Ahead

Regardless of the final legislative outcome, the direction of travel is clear: regulators are placing increasing scrutiny on payment practices and supplier protection.

Treasury teams that proactively assess the potential impact on liquidity, working capital, and supplier financing strategies will be better positioned to respond as the regulatory landscape evolves.

For organisations evaluating how the proposed reforms will affect their working capital strategy, now is the time to begin planning.

If you would like to discuss the implications of the proposed legislation or explore potential working capital solutions, please contact:

Daniel Smith

Director of Origination, Orbian

Or schedule a meeting directly:

https://calendly.com/daniel-smith-orbian/u-k-payment-term-legislation-orbian-s-flex-pay