Orbian Global Risk Perspectives – 2025

A Shift in Focus: Understanding the New Risk Landscape for Supply Chains

In early 2025, Orbian polled over 1,200 clients across 45 countries and 20 major industry sectors, from commodities to manufacturing, distribution to retail, on their current perceptions of key risk factors. This broader approach to risk replaces the ESG-focused assessments we’ve conducted for the past four years. The reasons for this shift will be clear.

The aim was to identify where client sentiment is most concentrated, and where businesses are recalibrating their risk awareness. What emerged was a clear reordering of risk priorities.

1. Geopolitical Risk – The Dominant Concern

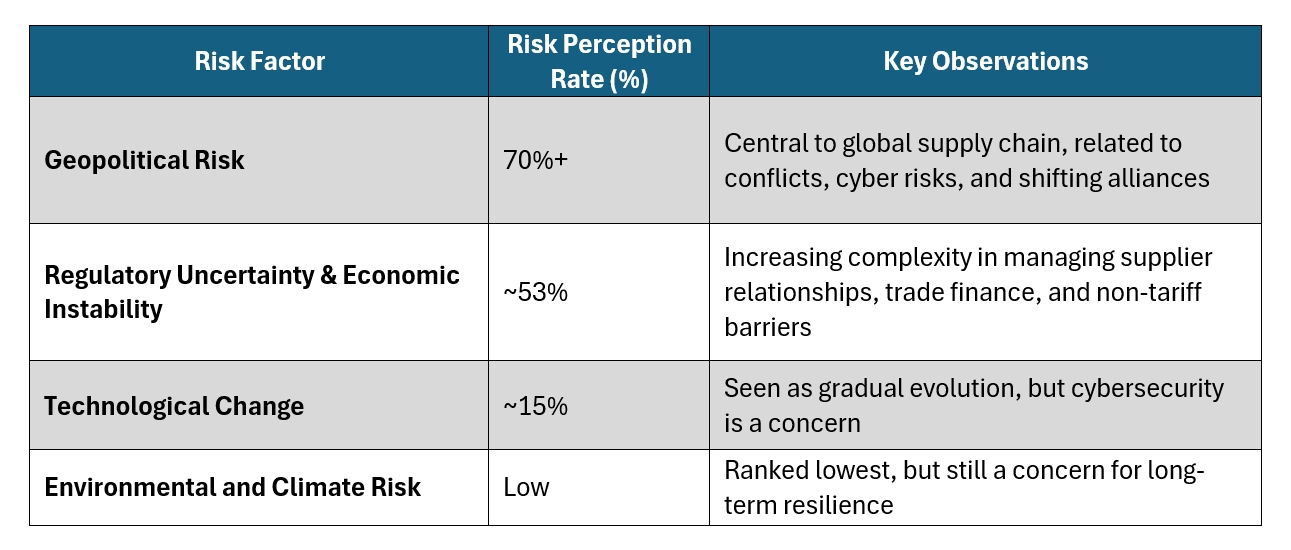

Across all geographies and sectors, Geopolitical Risk emerged as the top concern, cited by more than 70% of respondents as being of Very or Extremely Grave concern.

This aligns with ongoing global disruptions: shipping volatility in the Red Sea, political instability across trade corridors, and growing regulatory fragmentation between major economies. For multinational supply chains, exposure to geopolitical shifts is no longer peripheral,it is central.

The daily images of open conflict in Ukraine and Gaza represent only the surface level of these risk factors. Cyber warfare, foreign political interference and the re-emergence of nationalist interests are the factors impacting the “new BAU” for clients across the globe. Orbian’s SCF programs are evolving to meet these needs with region-sensitive structures, ensuring clients retain liquidity and flexibility amid shifting alliances.

2. Regulatory Uncertainty & Economic Instability – A Close Second

The second most cited area of concern was Regulatory Uncertainty and Economic Instability.

As highlighted in recent analysis on trade policy changes across the US, EU, and China, many companies now face increasing complexity in managing supplier relationships, cross-border compliance, and trade finance continuity. These challenges pre-dated the most recent escalation of tariff measures. Recent developments, from fiscal reform in Germany, to fluctuating central bank policies on both sides of the Atlantic, and a continuous ratchet of non-tariff barriers on global trade have made it increasingly difficult for clients to forecast costs, manage supplier obligations, or plan strategic shifts.

Supply chain financing must adapt accordingly. In our ongoing policy tracking, we note opportunities to assist clients facing regulatory transition costs, particularly in FMCG, Renewable Energy, and General Industrial sectors. Whether it is pre-shipment finance for ingredient reformulations or working capital solutions for infrastructure-linked demand spikes, the need for responsive financing tools is growing.

3. Technological Change – A Recalibrated Threat

Despite the current discourse around AI, automation, and robotics, only a small portion of respondents (~15%) considered Technological Change to be a Very or Extremely Grave concern.

This suggests a shift in perception. Many firms may no longer view technological disruption as an imminent threat, but rather as a gradual evolution, particularly where core logistics, manufacturing, and procurement processes remain people- and infrastructure-intensive.

That said, cyber risk remains a notable sub-theme. Across both survey rounds, clients indicated moderate concern over cybersecurity resilience. Orbian continues to enhance protections and digital resilience within our SCF systems, while advising clients on continuity strategies in case of supply chain IT disruption.

4. Environmental and Climate Risk – The Lowest-Ranked Concern

Environmental risk, including climate-related supply disruptions, ranked lowest among the four main categories.

This is a notable shift, given the backdrop of wildfires, extreme weather, and regulatory acceleration on climate goals. However, the survey indicates that most respondents believe their current operations are not immediately vulnerable to climate events.

While climate remains a long-term concern, particularly as it intersects with regulation and insurance, many clients have deprioritized it relative to more immediate operational and financial risks.

Nonetheless, policy developments across Germany, the US, and broader EU markets suggest that regulatory mandates on sustainability and supply chain disclosure are likely to increase in scope.

Supply Chain Support – A Clear Opportunity for Improvement

One additional question we asked was: To what extent do you feel supported in your supply chain risk arrangements?

The average response was 2.9 out of 5, suggesting significant room for improvement.

This insight reinforces Orbian’s ongoing work to position SCF not just as a funding mechanism, but as a resilience strategy. As global supply chains grow more volatile, clients are seeking partners that can help them transition from vulnerable to resilient, and ultimately toward anti-fragile systems capable of thriving in disruption.

In order to assist our clients as they navigate these new challenges, we will offer new planning tools including:

- Scenario-based financing readiness

- Regional and sector-specific risk planning

- Enhanced onboarding for suppliers in high-risk regions

- Interest rate management and “on-demand” liquidity availability

The 2025 Orbian Risk Survey highlights a marked shift in client priorities, from ESG to existential risk. Geopolitical fragmentation, regulatory volatility, and macroeconomic instability have become the defining challenges of the global supply chain landscape.

Orbian is committed to supporting clients through these transitions—helping them mitigate uncertainty, adapt to shifting policy environments, and seize opportunities for structural resilience. Our goal is not only to provide liquidity, but to help clients build systems that can anticipate, absorb, and evolve with risk.